Market Outlook Workshop Speakers Offer Insight Into Possible Recession, Ongoing Supply Chain Issues and Political Impacts for 2023

From the positive impacts of the Infrastructure Investment and Jobs Act (IIJA) to the negative repercussions from the war in Ukraine, external forces continue to shape an uncertain future.

#controls #water-wastewater

Share

VMA held its annual Market Outlook Workshop in conjunction with the Hydraulic Institute (HI) in August, reviewing what’s happened with the global market since the 2021 event. The focus again was how the U.S. and Canadian end users served by the industrial valve and pump industries have been impacted and may be impacted going forward. Joined by a slate of experts from end use market industries and financial and economic consulting firms, the two-day event, open to VMA and HI members only, covered pending and new legislation, Covid-19 rebounds to the supply chain and overall economy, and dove into some predictions for the next few years.

The huge impact Covid-19 had and continues to have on all facets of industry is still creating unrest in global markets, as 2022 winds down and we try to prepare for ongoing uncertainties in 2023. Output is slowing in the U.S. and globally as backorders are fulfilled from supply chain and manufacturing disruptions of the past two years. Geopolitical issues in Ukraine and Russia, as well as tensions between China and Taiwan, continue to impact the global economy and will linger into 2023. VALVE Magazine was able to attend and found the following key takeaways from the speakers during the recent workshop.

GLOBAL ECONOMIC TRENDS & OUTLOOK

Returning speakers Simona Mocuta (State Street Global Advisors chief economist), Michael Halloran (Robert W. Baird associate director of research) and Connor Lokar (ITR Economics speaker and senior forecaster) all presented their perspectives and predictions for the coming year. Overall, they were very much aligned on their predictions that 2023 is likely going to be mixed for many industries. Lokar described the labor market as “shades of gray,” with a slowdown in job postings and turnover as well. But, he expects labor cost pressure to improve next year. “It’s a lagging economic indicator, and I don’t think you’re going to feel great, but you won’t be as strained as the last couple of years,” he said.

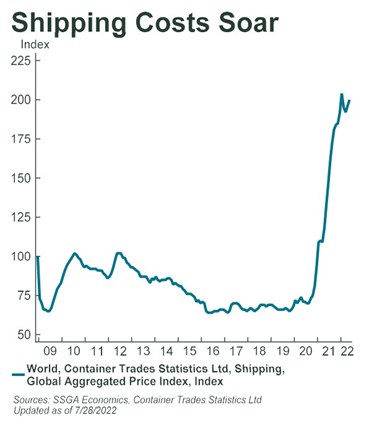

Mocuta agreed with Lokar that inflation is going to be moderate, and she believes that a disinflationary episode especially in manufacturing of goods is coming, with prices declining in some areas but not all. “Shipping is one area where I see genuine correction because it’s been too out of the norm,” she said. “Now that inventory building is happening again, things should start normalizing, but (lower prices) isn’t something I’d expect to see broadly speaking.”

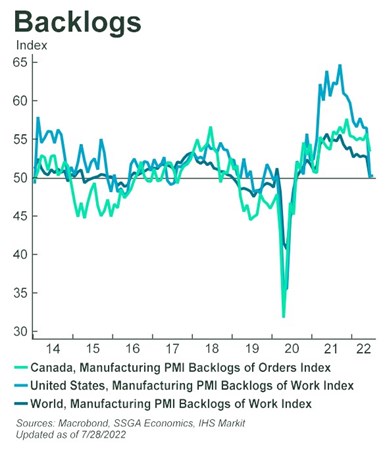

When asked how unusual it is to be entering a recessionary period when companies have had historic backlogs, Halloran said this is very industry dependent. “In 2008, it happened in the back half of the year, but energy companies had record years in 2009,” he replied. “Any time you come out of a recession you have people overcorrect on the capacity side or the workforce side, so as you come out you have supply chain challenges and labor constraints. In the past couple of years, you’ve had this on steroids because of how quick the pullback was and how quickly industry responded.” But, when you add in geopolitical concerns and ongoing supply chain challenges, “you get to backlog levels and inflationary concerns you’ve never had before,” he said.

Halloran believes industries that could grow next year include energy, automotive, commercial construction, and utilities with heavy infrastructure ties — location dependent — with the passing of the Infrastructure Investment and Jobs Act (IIJA).

Mocuta clarified that automotive growth won’t come from demand, but supply constraints due to long backlogs from chip shortages throughout the pandemic. “I expect some of the backlogs to completely clear from other industries next year, but auto manufacturing backlogs could continue. Lokar said the indicators he monitors suggest growth in energy, non-residential construction and water/wastewater, with automotive also being a possibility.

The conversation turned to the chip shortage that impacted a wide swath of electronic manufacturers but hit the automotive market particularly hard. The political tension between China and Taiwan can only exacerbate this. “I look at the CHIPS Act, and while it’s a good step, it’s a drop in the bucket for what it costs for one foundry to be built — and they only have a 5-6 year typical useful life. I do think there’s some reshoring potential, but I think it’s gradual.”

He said as companies and people think about the economics of building capacity here in the U.S., companies may hold to cheaper offshore options until they are forced to move production here. And, even with $50 billion in additional investments in American semiconductor manufacturing, the capacity this would create will only increase U.S. market share of chips from less than 2% to up to 10% in the next decade.

The IIJA will certainly help local utilities and construction companies that focus on projects like these, but there is still much to be learned about where the dollars will be allocated. Lokar pointed out that even if the dollars are awarded to local projects, there may still be an imbalance in the required labor and equipment to execute the projects. What follows are short summaries of specific industry outlooks from the speakers.

PROCESS CONTROLS

Mike Halloran’s session focused on markets most relevant to VMA and HPI members. Process markets such as oil and gas and chemical companies, infrastructure and municipal water and wastewater agencies and mining should see growth volume continuing in 2023. The power market will likely have small growth to slight decline, particularly in wind and solar, as well as coal and nuclear. That said, Halloran seemed a little bullish on the return of nuclear energy.

“Nuclear provides that baseload and is the cleanest of the alternatives… (but the public’s) perception is to look at big disasters and what it could mean. Yes, there is some risk, but today’s nuclear power plants are so much more sophisticated. There’s a viable opportunity for that to be coming to the forefront.” He continued, “New power plants take a long time to build so I don’t think that’s a near-term benefit, but on the five- to 10-year horizon, it’s a good thought process.” As the world sees warming temperatures and the power grid is more stressed every day, nuclear could have another small renaissance.

Halloran’s predictions for short-cycle industrial show healthy demand but the outlook is challenging due to deceleration curves, but he sees stronger market dynamics in the oil and gas sector than there have been in more than a decade for midstream and upstream, and for downstream and chemical plants due to market disruption and underinvestment in new infrastructure and MRO business. Water and wastewater municipal budgets are healthy, and with the passage of IIJA, this should continue into the near-term future.

MINING

As the world grapples with the extent to which it can transition to clean energy and how quickly, the demands on critical materials like copper, lithium, cobalt and nickel continue to rise, said Doug Anderson of PwC. There has been underinvestment, leading to supply shortfalls that put the energy transition to these alternatives at near-term risk. And by 2040, he predicts that critical minerals for clean energy will surpass $400 billion — equivalent to the coal market today.

“Demand projections to meet net-zero energy shows demand exceeding both operating capacity and what is currently under construction by a significant amount,” said Anderson. “Combined with the fact that production of many of the minerals concentrated in just a few countries, there is significant risk from not just capacity but geopolitical risks and economic resource scarcity among others.”

According to the USGS, cobalt, graphite, lithium and manganese are the most important mineral commodities in battery technology. Resource scarcity is key here because in 2019 the U.S. relied on foreign sources for 100% of its graphite and manganese needs, 61% of cobalt, and more than 50% of lithium. Countries with the biggest concentration of these minerals are China, Australia, South Africa, Indonesia and the Congo. Mexico, with the tenth largest global reserve of lithium recently nationalized its lithium resources and outlined the possibility for the state to take over other strategic mineral reserves — forcing out private investment in the country’s mining industry of these critical products.

The shift to net zero will require even more mining, particularly to support the battery needs for solar and wind power, electric vehicles and grid-scale batteries for energy storage. The electric vehicle market alone today requires 209 kg per vehicle of critical minerals content, while conventional vehicles require just 35 kg. That disparity means opportunity for miners across the globe.

The key takeaways from Anderson for the valve and pump industry were:

- Mining companies with a position in critical minerals should outperform their peers. They should also look to own more of the supply chain, partner more with their OEM customers, and evaluate development models around shared infrastructure to lower upfront costs and shorten timelines.

- The financial strength of the mining industry will be key for them to deploy capital, and significant capital will be required for the transition to clean energy.

- Mergers and acquisitions (M&A) will reshape the current top 40 companies, with high volatility in the short- to medium-term based largely on geopolitical risk.

- As mining companies strengthen their environmental, social and governmental (ESG) commitments, they will ask more of their suppliers.

Anderson concluded by saying while the outlook for mining is strong, there is a significant transition occurring which presents the industry an opportunity to continue to support mining customers and take advantage of the sector’s growth, coming out stronger in the long term.

WATER & WASTEWATER

The IIJA passage will have a substantive impact on our country’s water and sewer system infrastructure, with $55 billion allocated for water infrastructure. Other funds for systems resiliency, ports and waterways of nearly $20 billion will also positively impact the industry. And there is still money being allocated from the American Rescue Plan that was signed in March 2021, with $350 billion dispersed to state and local governments over five years. But according to speaker Tom Decker, the American Society of Civil Engineers calculates an investment need of $109 billion a year, so there is still a gap in what’s required.

Restrictions put into place over the previous decades to preserve water haven’t been effective due to ongoing drought conditions and the driest two decades in more than 1200 years in California. Two reservoirs on the Colorado River that feed water to much of the western U.S. will not be able to generate power if the water levels drop by another 32 feet. To help combat this, reclamation projects are taking off. A goal was set in Los Angeles to retrofit the Hyperion wastewater treatment plant to a reclamation and reuse facility to supply up to 35% of the city’s water needs in the future. There are dozens of other projects like this in various stages of development, as well as desalination plants and other groundwater treatment systems.

Other challenges for this sector include long lead times for equipment, pipe prices being up as much as 48%, and labor challenges indicate that this sector has great opportunity but also many challenges not just for 2023 but potentially for many years ahead. But the news for pump and valve companies is positive — 15% of utilities indicated in a recent poll they will be purchasing equipment in the coming year.

HYDROPOWER

Only 80 gigawatts (GW) of today’s U.S. power generation capacity comes from hydropower, but this is approximately 40% of U.S. renewables according to Tim Oakes of Kleinschmidt Associates. In Canada, that number rises to 60% of electricity output. And pumped storage represents over 90% of grid storage in the U.S. today, with another 50 GW currently in development. Below are key findings from a poll produced by Kleinschmidt Associates in partnership with the Hydropower Foundation and Ontario Waterpower Association.

- In the next three years, there will be many changes, including expected increase in value for hydropower.

- There will be continued investment into existing projects including generators, turbines and gates.

- Expect an increase in direct power purchase agreements and increased bundling and collocating with other renewables, and in greenfield pumped storage development.

- While an increase in incentive programs is expected, there will also be an increase in decommissioning activity due to project economics, environmental considerations and dam safety. Decommissioning projections increased substantially from 12.5% to 37.5% in the U.S. and 28.6% to 57.2% in Canada.

When asked about the biggest threats or challenges the hydropower industry faces today, respondents said low energy prices, climate change, regulatory burdens, high development costs and the perception of hydropower relative to other renewables were their biggest concerns.

OVERALL PREDICTIONS

As you can see, the coronavirus pandemic is still greatly affecting the outlook for market conditions for 2023 and beyond. There are bright spots in the near term for the valve and pumps market, but also many unknowns remain. Political unrest in Europe and Asia impacts all facets of our economy in some way, and labor shortages remain in the U.S. The fear of a recession lingers, but the overriding outlook for the industries covered looks more positive than negative.

Remaining session information is available on valvemagazine.com including more details from speakers on: packaging, tissue and paper, the chemical industry and construction outlook.

RELATED CONTENT

-

Direct-Sealing Diaphragm Valves Offer Novel Approach

As modern industries such as hydrogen electrolysis and biotech make dramatic technical advances, engineers and researchers must sometimes turn to nontraditional process control systems.

-

Best Practices in Pressure-Relief Valve Maintenance and Repair

In their presentation at the Valve Repair Council Repair Meeting & Exhibition, Nov. 1 and 2, 2012, in Houston, Bob Donalson and Kevin Simmons of Pentair Valves & Controls shared valuable information about maintenance and repair programs for pressure-relief valves.

-

Solenoid Valves: Direct Acting vs. Pilot-Operated

While presenting in a recent VMA Valve Basics 101 Course in Houston, I found myself in a familiar role: explaining solenoid valves (SOVs) to attendees. (I work with solenoids so much that one VMA member at that conference joked that I needed to be wearing an I Heart Solenoids t-shirt). During the hands-on “petting zoo” portion of the program, which involves smaller groups of attendees, one of the most frequently asked questions I get from people came up: What’s the difference between direct-acting and pilot-operated SOVs, and how do we make a choice?

Unloading large gate valve.jpg;maxWidth=214)